All Categories

Featured

Table of Contents

In the event of a gap, outstanding plan loans in extra of unrecovered price basis will undergo regular earnings tax. If a plan is a modified endowment agreement (MEC), policy finances and withdrawals will certainly be taxable as normal earnings to the degree there are profits in the plan.

Tax regulations are subject to alter and you ought to get in touch with a tax specialist. It is essential to keep in mind that with an exterior index, your plan does not straight join any type of equity or set earnings financial investments you are denying shares in an index. The indexes offered within the plan are constructed to keep track of varied segments of the united state

These indexes are benchmarks just. Indexes can have various constituents and weighting methods. Some indexes have multiple versions that can weight components or might track the influence of returns in different ways. Although an index might influence your passion attributed, you can not buy, straight join or receive returns repayments from any one of them through the policy Although an external market index may affect your rate of interest credited, your policy does not straight take part in any kind of stock or equity or bond investments.

This web content does not apply in the state of New York. Warranties are backed by the monetary stamina and claims-paying capacity of Allianz Life Insurance Coverage Business of North America. Products are released by Allianz Life Insurance Coverage Business of North America, 5701 Golden Hills Drive, Minneapolis, MN 55416-1297. .

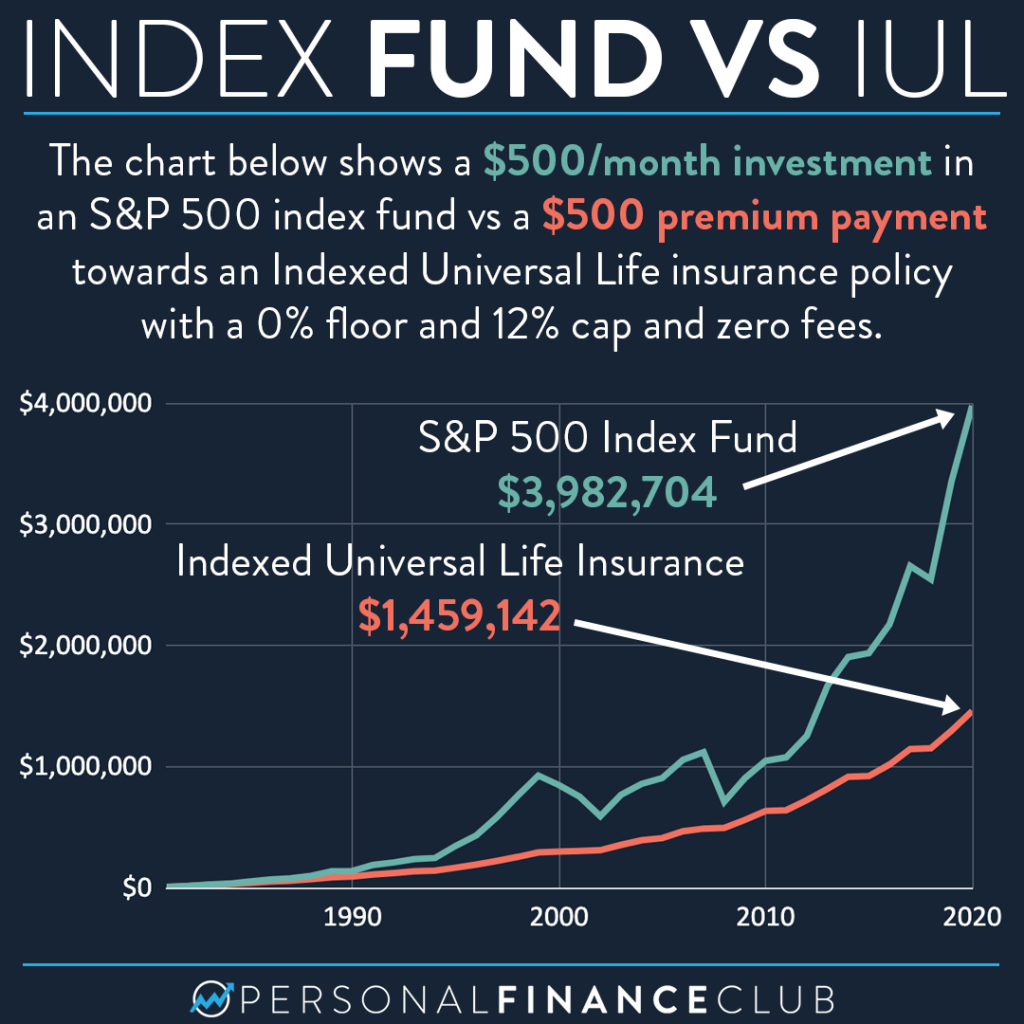

Shield your enjoyed ones and save for retirement at the exact same time with Indexed Universal Life Insurance Coverage. (High cash value Indexed Universal Life)

What types of Indexed Universal Life Tax Benefits are available?

HNW index global life insurance policy can assist gather money value on a tax-deferred basis, which can be accessed during retired life to supplement revenue. (17%): Policyholders can often borrow versus the money value of their plan. This can be a resource of funds for different demands, such as spending in an organization or covering unanticipated expenses.

The death benefit can assist cover the prices of finding and training a substitute. (12%): Sometimes, the money value and survivor benefit of these policies might be secured from financial institutions. This can give an extra layer of financial safety. Life insurance policy can also assist reduce the threat of an investment profile.

What is the difference between Iul Calculator and other options?

(11%): These policies supply the potential to earn rate of interest linked to the performance of a securities market index, while also providing an ensured minimum return (Indexed Universal Life investment). This can be an appealing alternative for those looking for growth capacity with disadvantage security. Resources for Life Study 30th September 2024 IUL Survey 271 respondents over 1 month Indexed Universal Life insurance policy (IUL) might appear complicated initially, but understanding its mechanics is essential to comprehending its full potential for your financial planning

If the index gains 11% and your involvement rate is 100%, your cash worth would be credited with 11% rate of interest. It is essential to keep in mind that the optimum interest attributed in a given year is capped. Allow's state your picked index for your IUL policy got 6% from the start of June throughout of June.

The resulting rate of interest is included to the cash value. Some policies calculate the index acquires as the sum of the adjustments for the period, while other plans take an average of the everyday gains for a month. No rate of interest is attributed to the money account if the index decreases rather than up.

Who are the cheapest Iul Insurance providers?

The price is established by the insurance provider and can be anywhere from 25% to greater than 100%. (The insurer can likewise alter the engagement price over the lifetime of the policy.) If the gain is 6%, the engagement rate is 50%, and the current cash value total amount is $10,000, $300 is added to the cash value (6% x 50% x $10,000 = $300). IUL policies commonly have a floor, commonly set at 0%, which shields your cash value from losses if the market index does adversely.

This provides a degree of safety and security and satisfaction for insurance holders. The interest credited to your money worth is based upon the efficiency of the selected market index. Nonetheless, a cap (e.g., 10-12%) is typically on the optimum interest you can earn in a given year. The part of the index's return credited to your money worth is established by the participation price, which can differ and be adjusted by the insurance business.

Store about and contrast quotes from different insurance policy business to locate the best plan for your demands. Before choosing this type of plan, guarantee you're comfy with the possible fluctuations in your money value.

Who provides the best Iul Calculator?

By contrast, IUL's market-linked money worth development uses the capacity for higher returns, specifically in beneficial market problems. This potential comes with the risk that the stock market performance might not deliver continually stable returns. IUL's flexible premium payments and flexible survivor benefit offer flexibility, interesting those looking for a policy that can advance with their transforming economic conditions.

Indexed Universal Life Insurance Policy (IUL) and Term Life Insurance coverage are various life plans. Term Life insurance policy covers a details period, commonly in between 5 and 50 years. It only provides a death advantage if the life guaranteed dies within that time. A term policy has no cash money value, so it can't be made use of to offer lifetime advantages.

It is ideal for those looking for temporary defense to cover particular economic responsibilities like a mortgage or youngsters's education and learning costs or for business cover like investor security. Indexed Universal Life (IUL), on the other hand, is an irreversible life insurance policy plan that provides coverage for your whole life. It is a lot more expensive than a Term Life policy since it is created to last all your life and provide a guaranteed money payment on death.

How does Iul Policyholders work?

Picking the appropriate Indexed Universal Life (IUL) plan is concerning locating one that straightens with your economic objectives and take the chance of tolerance. An educated economic advisor can be very useful in this process, directing you with the intricacies and guaranteeing your selected policy is the best suitable for you. As you research buying an IUL policy, keep these crucial factors to consider in mind: Recognize just how credited rate of interest are linked to market index efficiency.

As laid out previously, IUL plans have different charges. Understand these expenses. This determines exactly how much of the index's gains add to your money value growth. A higher price can increase possible, but when comparing plans, review the cash money worth column, which will certainly aid you see whether a greater cap price is much better.

How do I get Indexed Universal Life Growth Strategy?

Research study the insurance firm's financial scores from firms like A.M. Finest, Moody's, and Criterion & Poor's. Various insurance firms supply variants of IUL. Collaborate with your adviser to comprehend and locate the most effective fit. The indices connected to your policy will directly affect its efficiency. Does the insurer supply a variety of indices that you intend to line up with your investment and danger account? Flexibility is very important, and your plan ought to adjust.

{kind=link}

Latest Posts

Equity Index Universal Life Insurance

Life Insurance Tax Free Growth

Iul Vs Roth Ira