All Categories

Featured

Table of Contents

The plan gains value according to a taken care of timetable, and there are fewer fees than an IUL plan. A variable plan's cash money value may depend on the efficiency of certain supplies or other protections, and your premium can likewise transform.

An indexed global life insurance policy policy consists of a fatality benefit, as well as a component that is linked to a securities market index. The money value growth depends upon the performance of that index. These policies offer higher potential returns than various other types of life insurance policy, along with higher dangers and extra charges.

A 401(k) has more investment choices to pick from and might come with a company suit. On the various other hand, an IUL includes a death advantage and an extra cash value that the insurance policy holder can obtain against. They also come with high premiums and fees, and unlike a 401(k), they can be terminated if the insured stops paying into them.

How long does Indexed Universal Life Plans coverage last?

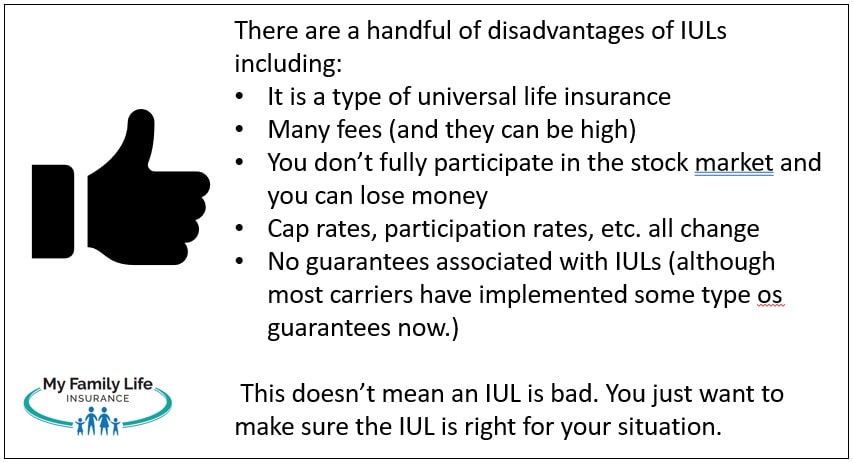

These plans can be much more complicated compared to other kinds of life insurance policy, and they aren't necessarily ideal for every financier. Speaking to a knowledgeable life insurance policy representative or broker can assist you decide if indexed universal life insurance policy is a good suitable for you. Investopedia does not supply tax obligation, investment, or monetary services and guidance.

Your existing web browser might restrict that experience. You may be using an old internet browser that's unsupported, or setups within your browser that are not suitable with our site.

How do I apply for Flexible Premium Indexed Universal Life?

Currently using an updated internet browser and still having difficulty? Please offer us a call at for additional assistance. Your present internet browser: Discovering ...

Your economic circumstance is distinct, so it is very important to discover a life insurance policy item that satisfies your details needs. If you're looking for life time coverage, indexed universal life insurance coverage is one alternative you may intend to take into consideration. Like various other permanent life insurance coverage items, these plans allow you to develop cash worth you can touch throughout your lifetime. Indexed Universal Life for retirement income.

That suggests you have extra lasting growth potential than a whole life plan, which supplies a set rate of return. Generally, IUL policies stop you from experiencing losses in years when the index sheds worth.

Nevertheless, understand the benefits and negative aspects of this product to figure out whether it aligns with your financial objectives. As long as you pay the premiums, the policy remains in pressure for your entire life. You can accumulate cash worth you can use during your lifetime for numerous financial demands. You can adjust your costs and fatality benefit if your circumstances transform.

How long does Tax-advantaged Iul coverage last?

Permanent life insurance coverage policies often have greater first costs than term insurance, so it might not be the best option if you're on a limited budget plan. IUL interest crediting. The cap on rate of interest credit histories can restrict the upside possibility in years when the securities market performs well. Your plan might lapse if you take out also huge of a withdrawal or plan funding

With the capacity for even more durable returns and adjustable settlements, indexed global life insurance coverage may be an option you want to think about., that can evaluate your individual scenario and give customized insight.

Possession and tax diversification within a portfolio is enhanced. Pick from these products:: Provides lasting development and income. Perfect for ages 35-55.: Deals adaptable protection with moderate cash worth in years 15-30. Perfect for ages 35-65. Some points clients should consider: For the fatality benefit, life insurance policy items bill costs such as death and expenditure risk fees and surrender charges.

Policy lendings and withdrawals may create a negative tax obligation outcome in the occasion of lapse or policy surrender, and will lower both the abandonment worth and fatality benefit. Customers need to consult their tax obligation expert when thinking about taking a plan funding.

What does Iul Premium Options cover?

It needs to not be considered investment guidance, neither does it constitute a recommendation that any person take part in (or refrain from) a specific training course of action. Securian Financial Group, and its subsidiaries, have an economic interest in the sale of their items. Minnesota Life Insurance Policy Business and Securian Life Insurance Policy Firm are subsidiaries of Securian Financial Team, Inc.

IUL can be utilized to conserve for future requirements and give you with a home mortgage or a secure retirement planning automobile. And that's on top of the cash money swelling amount paid to your loved ones. IUL provides you money worth development in your life time with stock market index-linked investments yet with funding defense for the remainder of your life.

To comprehend IUL, we first require to damage it down right into its core components: the cash worth element the survivor benefit and the cash money value. The survivor benefit is the amount of money paid to the insurance holder's beneficiaries upon their passing away. The plan's cash-in worth, on the other hand, is an investment part that expands gradually.

How can Iul Death Benefit protect my family?

Whilst plan withdrawals are beneficial, it is important to monitor the policy's efficiency to guarantee it can sustain those withdrawals. Some insurance firms also restrict the amount you can withdraw without reducing the death advantage amount.

The economic stability needed focuses on the capacity to take care of exceptional repayments easily, although IUL policies provide some flexibility.: IUL policies permit adjustable premium repayments, providing policyholders some flexibility on exactly how much and when they pay within set limits. Regardless of this versatility, regular and ample funding is vital to keep the plan in great standing.: Insurance holders need to have a stable income or enough savings to guarantee they can satisfy exceptional needs over time.

Who offers flexible Guaranteed Indexed Universal Life plans?

You can choose to pay this interest as you go or have the rate of interest roll up within the policy. If you never pay back the finance during your lifetime, the fatality advantages will be lowered by the amount of the impressive car loan. It indicates your beneficiaries will receive a lower quantity so you may want to consider this prior to taking a plan financing.

It's vital to monitor your cash worth equilibrium and make any kind of required adjustments to stop a policy gap. Life plan projections are an essential device for understanding the possible performance of an IUL plan. These estimates are based on the predicted rate of interest prices, charges, settlements, caps, participation price, rate of interest rates utilized, and fundings.

{kind=link}

Latest Posts

Equity Index Universal Life Insurance

Life Insurance Tax Free Growth

Iul Vs Roth Ira